-

About Jordan

About Jordan

-

Client Testimonials

Client Testimonials

-

Selling My Home

Selling My Home

-

Buying a Home

Buying a Home

-

Contact Jordan

Contact Jordan

About Jordan

Client Testimonials

Selling My Home

Buying a Home

Contact Jordan

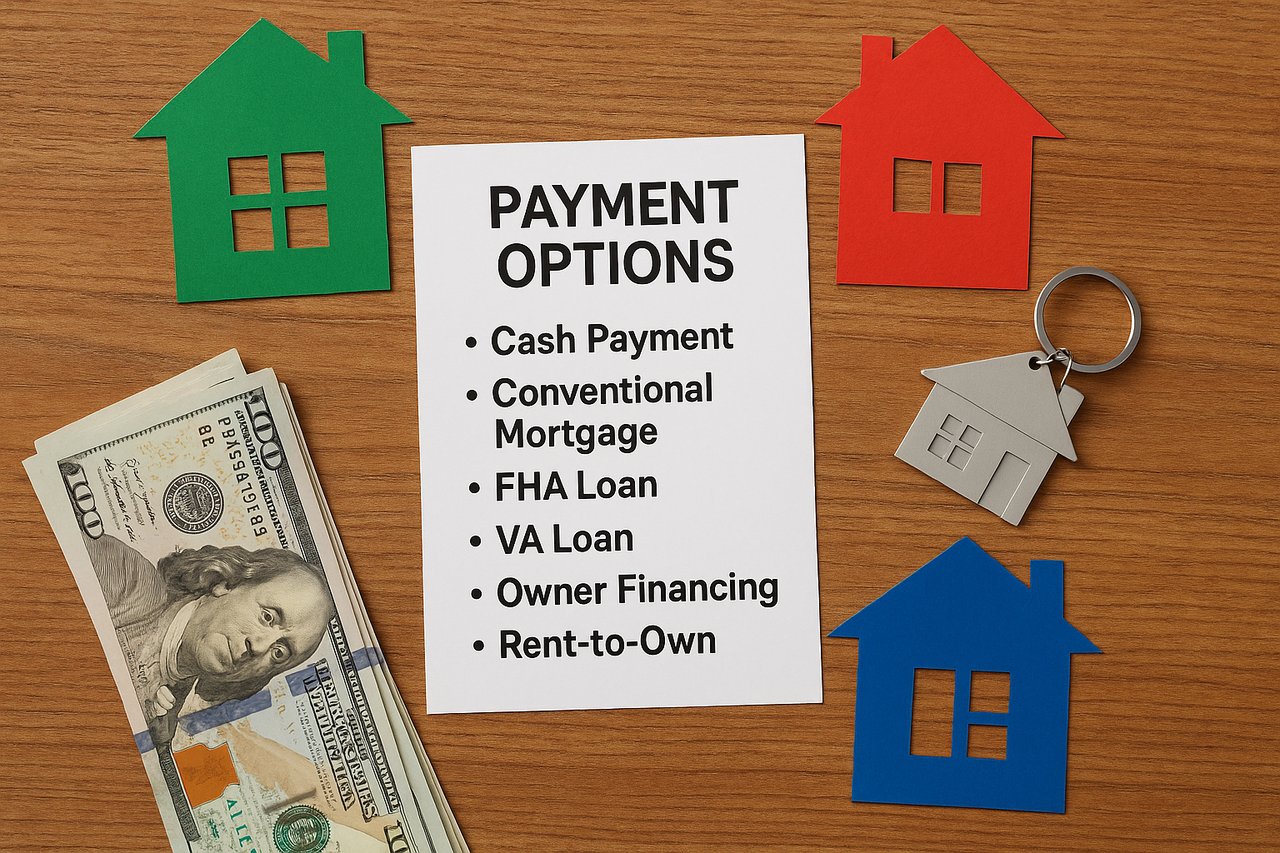

Real estate is one of the most significant investments most people will make in their lifetime. Whether you're buying your first home, investing in property, or expanding your real estate portfolio, understanding your payment options is essential. The right financing strategy can help you save money, secure better terms, and close deals more confidently.

In this post, we’ll walk through the most common payment methods in real estate, their benefits, and how to decide what works best for your situation.

Overview:

A full cash purchase means the buyer pays the entire cost of the property upfront without financing.

Pros:

Faster closing process

No mortgage interest or lender fees

Stronger negotiating power

Cons:

Ties up a large amount of capital

Missed opportunity to leverage financing for better liquidity

Best for:

Buyers with substantial savings, investors seeking quick deals, or competitive offer situations.

Overview:

A conventional loan is a mortgage not insured by the government, usually offered by private lenders like banks and credit unions.

Pros:

Flexible loan terms (15, 20, or 30 years)

Lower interest rates with good credit

Widely accepted in most transactions

Cons:

Requires good credit and a stable income

5%–20% down payment often needed

PMI (Private Mortgage Insurance) required if down payment is less than 20%

Best for:

Homebuyers with stable income and credit looking for standard residential property financing.

Overview:

An FHA loan is a government-backed mortgage designed to help first-time or low-income buyers.

Pros:

Lower down payment (as low as 3.5%)

More lenient credit requirements

Cons:

Mortgage insurance premiums (MIP) required

Property must meet FHA appraisal standards

Best for:

First-time homebuyers or those with lower credit scores and smaller down payments.

Overview:

Available to eligible veterans, active-duty service members, and some spouses.

Pros:

No down payment required

No PMI

Competitive interest rates

Cons:

Only available to qualified military borrowers

Property must be VA-approved

Best for:

Eligible military personnel and veterans looking for affordable financing.

Overview:

The buyer pays the seller directly in installments, often bypassing traditional lenders.

Pros:

Flexible terms

Useful for buyers who can’t qualify for a traditional loan

Cons:

Often higher interest rates

Requires legal vetting and careful documentation

Best for:

Buyers with non-traditional income or credit issues, or niche property sales.

Overview:

Buyers rent the property with the option to purchase after a set period.

Pros:

Lock in purchase price

Time to improve credit or save for a down payment

Cons:

Higher monthly payments

Risk of losing premium payments if the purchase doesn't happen

Best for:

Buyers who need time to prepare financially but want to commit to a specific home.

Your best payment method depends on:

Your credit score and income stability

Available savings for a down payment

How long you plan to own the property

Whether the property is for personal use or investment

Consulting a real estate agent or mortgage advisor can help you evaluate your options, understand local market trends, and navigate financing paperwork effectively.

Final Thoughts

Real estate doesn't have a one-size-fits-all payment strategy. Whether you're going the traditional route with a mortgage or exploring creative financing like rent-to-own or owner financing, knowing your options helps you make smarter, more confident decisions.

Want help getting started with financing or connecting with a lender? Let us know—we’re here to help you navigate the path to homeownership.

Browse active listings in the area or contact us for off-market listings.

Have an expert help you find out what your home is really worth.